繁体中文

繁体中文

Abstract:First batch of U.S. “nominal” Bitcoin ETFs, BITO and BTF, finally launched in October 2021. The market has set off a craze, leading CME Bitcoin Futures open interest to rise 49% and reaching historical high of $5.45 billion in net worth. Till Nov.2, BITO (ProShares) has achieved an exposure value of over $1.28 billion, nearly 24 times greater than BTF (Valkyrie) which launched merely 2 days later, demonstrating a huge market favor for “early birds”.

▶ Comparing Filings of 6 Futures ETFs

- Futures ETFs share similar properties, competition may lie in fees (i.e. 0.95% of BITO and 0.65% of VanEck), and directions like short exposure.

- Actively management include rolling and diversification. BITO and BTF held 34.35% and 49.97% of Bitcoin Futures respectively; the latter held front-month contracts only.

▶ Futures ETFs VS Spot Products (ETPs/ETNs):

- Futures ETFs allowed two-way cross-market trading, enabling flexible strategies for institutional arbitragers.

- Futures ETFs provides liquidity expansion that frees from circulating of Bitcoins.

- CME position has limits of 4,000 for front-month and 5,000 for overall.

- Potential contango risks in futures may cause extra internal costs, 10.91% for current annualized spread, and an average of 5%-10% overall.

- A 25%-35% tax rate applies for unrealized gain in futures, which is much higher than spot products.

We believe the launch of futures ETFs is a milestone for crypto industry and financial markets. It is a compromise SEC has made adapting to the heating market demand; more futures-based products are on the way. Additionally, futures ETFs may create a new channel for the discovery of Bitcoin’s fair value.

Looking forwardly, we consider the crypto asset management market will be facing a rat race that will lead to an increase in arbitraging activities in the short run due to product nature. In the long run, we believe Bitcoin futures ETFs could be the bridge to the launch of spot ETFs. Current gap could be a chance for those crypto-friendly countries in EU and Asia, especially the UK, Germany, Switzerland, Singapore, and Malaysia.

Author:

Huobi Research Institute | Han. Chen, Cyphever. Wang

I. Introduction

With the diffusion of cryptocurrencies, first “nominal” Bitcoin ETF in the U.S., BITO, has successfully launched. Before BITO, US companies have devoted tremendous resources pursuing support and approval from SEC. More than 10 reputed institutions applied for launching Bitcoin spot ETFs since 2017 while none succeeded. The launch of BITO implies that SEC has compromised to Bitcoin ETFs by approving futures-backed products.

Figure 1 Application record of US Bitcoin ETF

Source: Huobi Research

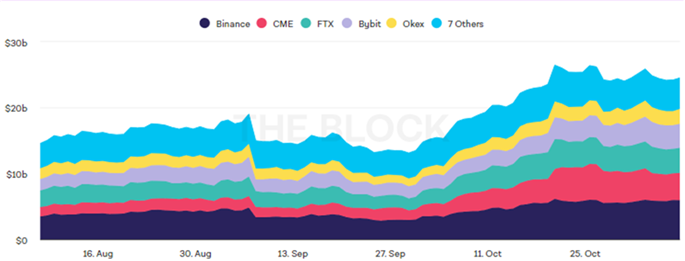

Since the launch of BITO and BTF, the open interest (OI) of CME Bitcoin futures soars around 49% to 17,433 contracts in 1 week with a value of approximately $5.45 billion, reaching historical high record. Meanwhile, the market value of Bitcoin futures elevates 14% to over $26 billion. OI dropped slightly later due to the breach of CME’s position limits and the approach of its first rollover. Data has illustrated market enthusiasm in the short run.

However, the “early birds” effect could be seen from ProShares’s listing prior to the launch of others. Meanwhile, the problem of position limits appears earlier. Comparing current existing 2 Bitcoin ETFs, we found that BITO (ProShares) achieved an exposure value over $1.28 billion, nearly 24 times greater than BTF (Valkyrie), while BTF’s inception date is only 2 days later than BITO. Similar market trend could also be spotted at the first launch of Purpose’s Bitcoin spot ETF’s in Canada.

Figure 2 Bitcoin futures OI

Source: TheBlock Data

Hence, will this trend remain? What further influence will it have upon the launch of more Bitcoin future ETFs? A deep dive into the product features is necessary to dig out the answers.

II. Difference, Pros & Cons

2.1 Difference between Future ETFs

▶ Fees Competition

We scanned statements filed by ProShares, Valkyrie, VanEck, BitWise, BlockFi and Direxion. Products seem to be similar at first glance, while key figures remain mysterious for those unlisted ones. However, we noticed that VanEck attempted to win over its rivals by applying a much lower fee of 0.65%. The creation unit size, which is the minimum size an Authorized Partner (AP) can purchase or redeem, is another difference. BITO has a lower required size of 10,000 shares, which brought about more flexibility to APs to arbitrage.

Table 1 Difference among ETFs already/about to launch

Source: Huobi Research

Direxion and Valkyrie have applied to provide products with new structure, but none progressed . Direxion intended to provide short exposure, while Valkyrie focused on elevating leverage exposure to 1.25. However, both applicants withdrew their applications merely 1 week after submission, implying strong concern of SEC on systematic risk.

▶ Management Philosophy

Another difference is the management philosophy of fund managers. The public has accustomed to perceive single-crypto aimed financial instruments as passively managed funds, such as GBTC or ETNs. However, futures ETFs require fund managers to actively adjust the turnover and exposure percentage; measurements may include both rolling strategy (switching the front to further-out month or investing to alternatives like bitcoin-related stocks or spot ETFs, ETPs) and collaterals position control.

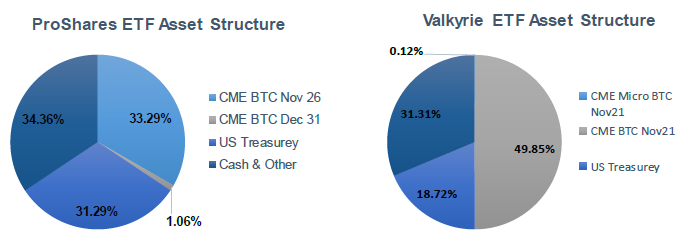

Figure 3 Portfolio Structure of BITO and BTF

Source: Official website, processed by Huobi Research

ProShares and Valkyrie held 34.35% and 49.97% of Bitcoin futures respectively in their ETF portfolios. ProShares invested 1.06% or $39.41 million into further-out contracts with expiration of Dec 31 2021, while Valkyrie held all front-month contracts with expiration in November. These differences will eventually reflect in the cost and performance of the 2 ETFs.

2.2 Difference Comparing to ETP/ETNs

▶ More Strategies Allowed for Institutions

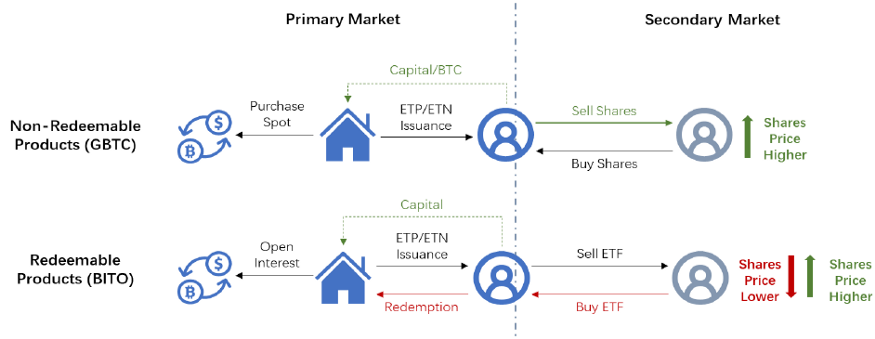

APs, mainly broker-dealers, are permitted to redeem their shares, which allowed institutions to apply more strategies.

ETF-liked products have 2 prices, NAV for primary market and market price for secondary market. NAV is calculated daily and less volatile than the market price. Therefore, premiums occur between 2 markets for the same product. In the case of a one-way traded product like GBTC showing above, investors can arbitrage when the price in secondary market is higher than the NAV of primary markets (this is called positive premium, and vice versa). However, if a negative premium occurs, ETPs are not allowed to take the advantage reversely; only defensive actions are allowed, such as borrowing GBTC on the secondary market for hedging. In such circumstances, two-way traded products like BITO allows buying from the secondary market at a lower price and redeeming them in the primary market with a higher payback.

Figure 4 Difference between non/redeemable products

Source: Huobi Research

The lack of two-way cross-market trading function will eventually cause low liquidity, with a further potential of causing “Death Spiral” like what GBTC is experiencing. In this term, futures ETFs offer greater arbitraging capability.

▶ Liquidity Expansion

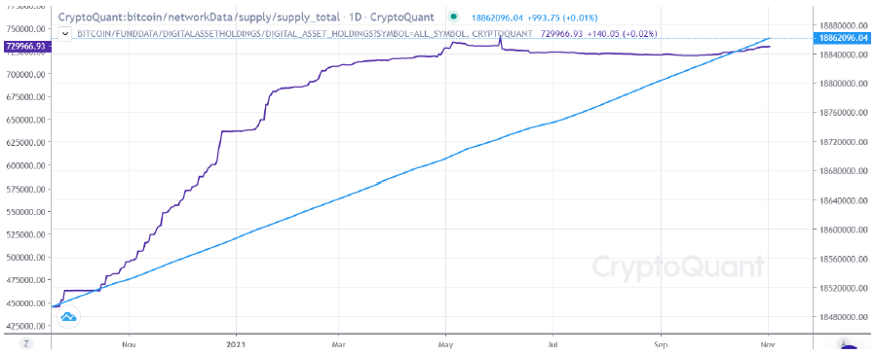

Spot products, including ETPs and ETFs, may not be sufficient to fulfill massive demand. According to Cryptoquant, spot-backed products including GBTC purchased 227k Bitcoins last year, approximately 69% of newly mined volume. Meanwhile, more institutions like Tesla are increasing Bitcoins inventory directly. On one hand, richer direct exposures to Bitcoins may generate huge spread for spot products, even a stockout under extreme market enthusiasm. On the other hand, future ETFs backed by USD has no such limits. Therefore, market liquidity is expanded.

Figure 5 Bitcoin issuance V.S. funds purchasing

Source: Cryptoquant, processed by Huobi Research

▶ CME Position Limits

Unlike spot ETFs, Bitcoin future ETFs are limited to their positions of contracts. Current rules of CME prevent “single investor” (i.e., an ETF) from holding over 4,000 front-month contracts, and 5,000 for an overall position of the same tick.

ProShares is currently facing such problem; it currently holds 3,885 front-month contracts and 122 further-month ones. Though ProShares has already applied to CME for remission, it could fail, but there is still a chance for its rivals.

▶ Contango Risks

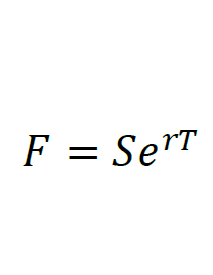

Contango risks emerge when the market price has strong expectations to rise, which could add higher premiums to contracts with longer expiration. According to spot–future parity’s simplified equality (Hull, John C.,2018):

S = price of spot market

F = price of future market, in this case, further-month contracts

r = risk-free rate

T = time period delivering forward contract

price of future-month contracts could always be higher in the case of long-only assumptions. When the expiration is closer, T→0, the spot-futures spread decreases. A fund like BITO will experience high rolling costs when extending the position’s expiration in such situation. Dating back, CME Bitcoin futures experienced long periods of contango, spreads are greater in bull markets (Feb to May, blue line minus yellow line).

The current spread between Nov and Dec is approximately -0.91%, assuming the spread continues, “Contango Bleeding” will occur; annualized rollover cost under current spread could reach -10.91%. Though future ETFs seem to charge low management fees, the internal costs of rolling are high. Average costs may reach 5%-10% for ETFs with frequently rolling requirements.

Figure 6 Historical view of CME bitcoin futures in different expiration

Source: TradingView, processed by Huobi Research

▶ Tax Burden

Another core issue is tax. According to the U.S. laws, commodity futures and their ETFs will: 1) account for any gain or loss as “marked to market” at the end of a year, that is to say investors must pay tax if they are in profit positions whether realized or not; and 2) 60% of gains are classified as long-term gains, which means higher tax rates will apply. Holding a position of BITO to a fiscal year end may generate tax expenses around 25%-35% of unrealized gains. Meanwhile, spot-anchored products like GBTC or ETNs do not have such strict requirements.

III. Significance of Future ETFs’ Launch

▶ Milestone for Crypto Industry and Financial Markets

It is a progress in terms of regulation’s adoption to crypto assets, since there has been seen more than 20 applications by 10+ famous funds in the past 7 years beginning 2014. The approval signals that BTC is officially recognized as a mature asset or commodity under current regulatory view. It also exposed BTC to a broader range of investors in mainstream, thus, a more liquid marketplace.

▶ SEC’s “Compromise” to Market Demand, More Future-based and Indirect ETFs on the Way

Over 15 Bitcoin-related ETFs submitted to SEC since 2020, only 2 applications passed. One was the futures-based product-BITO, the other is the crypto-linked stock-based product- the Volt Equity. This indicates that:

- crypto-based ETFs has strong market demand on both vendors and investors,

- US regulatory is still concerned with potential risks, including market manipulation and custody in spot-based products, but it has compromised to CME future-based and indirect exposure ones.

Therefore, more ETFs will be listed in the next few months within expectations.

▶ New Price Discovery Channel, US Exchanges Expand Influence in Crypto Industry

Crypto spot trading is still blocked out of major secondary financial markets, such as Nasdaq and NYSE, mainly because of price discovery efficiency. The launch of future ETFs offers a new price discovery channel, which allows more traditional funds to allocate with the upcoming ETFs launched. It is vital for Bitcoin to become a mainstream asset.

IV. Outlook

▶ A Rat Race

The current crypto asset management market mainly consists of trust funds, ETPs and ETNs. Futures ETFs charges a lower fee of 0.95%, compared to 2%+ of Grayscale or Bitwise, or nearly 1.5% of Coinbase trading fees. The rat race is upcoming between spot trusts and future ETFs.

Nevertheless, future-based ETFs will compete in fees, product design and futures rolling management ability. New product design is limited to leveraged ones, but short exposure may be the next battlefield.

▶ More Short-term Investors or Arbitragers

With scrutiny into the product itself, futures ETF provides an arbitrage exposure of Bitcoin rather than tracing spots. This product is better for arbitraging or hedging strategies rather than simply seeking betas. From tax perspective, futures ETFs are eligible for heavier tax burden by 25%-35% for unrealized gains. As a result, market participants are compelled to chase short-term investments, exactly as ProShares stated in its filings: “Investors shall expect quite a large portion of capital gains to be short-term”.

▶ Limit in the Short-run, the Bridge to Spot ETFs

The short-term impact has already been reflected on BTC’s price, indicating strong confidence in the crypto industry. This may not stay the same on the traditional side. Current exposure to Bitcoin has comparative facilities for market engagement, including exchanges, trust funds or even crypto-lending markets.Since futures ETFs do not provide direct exposure to Bitcoin, and there are still problems in rolling costs, position limits and taxes, etc., barriers will remain and thus impede for new market entry.

Futures-based products could be the bridge, providing market feedback and risk monitoring measurements for regulatory, and facilitating the launch of spot ones. Nonetheless, spot ETFs still have a long way to go, including fair price efficiency, market manipulation, premium caused by limited supply (for Bitcoins).

▶ Market is Hot, a Chance for Crypto-friendly Countries in EU and Asia

In the long run, we may see a raise in CME market share in crypto contract market, especially in terms of short exposure products launching.

Market demand for spot ETFs remains high, which may lead to more launch of spot products prior in the EU or Asia. We will keep an eye on the market movement in the UK, Germany, Switzerland, Singapore, and Malaysia.